South Africa—The Pecan Industry’s Next Paradigm Shift?

"Paradigm Shift: a dramatic change in the basic assumptions, ways of thinking and methodology that are commonly accepted by members of a specific community or group."

This aerial view shows several blocks of orchards, in various stages of maturity, outside of Hartswater, South Africa. (Photo by Dan Zedan)

Why mention this? Because over the past thirty-or-so years, the pecan industry has gone through a dramatic transformation. While it can certainly be argued that the development of high-yielding inshell varieties, modern agricultural and irrigation practices played a significant role in the movement of the industry into the 21st century, without the development of better cracking and sorting technology, the industry would not have been able to expand its markets to the rest of the world while continuing to supply its core domestic customer base.

Those technological advances led to new markets which in turn led to increased demand and new plantings. As such, it could be reasonably argued that the industry’s first paradigm shift occurred with the invention of the Champion/Meyer Pecan Crackers. Shellers no longer had to rely on hand sorting and cracking. Each cracker could easily process between sixty and ninety nuts per minute.

The next two paradigm shifts occurred in the 1980s with the advent of the Mexican pecan industry and the introduction of the Quantz Cracker. As the available supply of pecans continued to increase, the only thing that prevented expansion of the U.S. domestic market was the shelling industry’s inability to supply it with high quality shelled kernels.

The Quantz Cracker solved that problem. Each Quantz Cracker replaced ten Champion/Meyer Crackers. When combined with the latest sorting technology, labor costs dropped dramatically. By the early 1990s, many shellers began to develop a robust export market. However, when compared to the almond and walnut industries which export approximately 70 percent of their crop, the pecan industry still relied on the U.S. domestic market for the bulk of its sales.

Workers prepare the ground for the first shaking of the new crop. The mesh nets are used to capture the nuts to facilitate hand collection. (Photo by Dan Zedan)

The fourth paradigm shift occurred in the first decade of this century—the advent of China as a consumer of pecans.

Prior to 2007, the pecan industry could be easily explained as a large hourglass. At the top of the glass was the supply of both Mexican and U.S. pecans. At the bottom, the world’s pecan consumers. The constriction point? The U.S. shelling industry. All inshell, whether Mexican or American, had to pass through the U.S. shelling industry. While several U.S. sheller’s had begun selling inshell pecans to China in the early ‘90s, the industry only sold their excess inventory. By restricting sales to China, the shellers were able to control supply while protecting their contract prices. That ended in 2007.

With short walnut crops in both China and the U.S. and an ample supply of pecans, Chinese traders quickly shifted their buying from walnuts to pecans. Unable to get sufficient quantities of inshell from the shellers, traders soon realized that they could bypass the bottleneck and go directly to the growers. The resulting shift in pricing-power soon led to significant increases in returns to the grower, exports, meat prices and outside interest in the newly minted profitability of the pecan industry.

With the influx of new money came increased plantings, increased production and a significant increase in competition, not only in North America but also from overseas. By 2012, China was consuming almost 30 percent of the U.S. crop and accounted for 50 percent of U.S. pecan exports.[1] U.S. inshell sales to China brought in almost $227 million.[2] The only problem: supply. Every sale to China meant one less sale to a U.S. domestic customer.

The U.S. was not the only country to benefit from China’s entry into the pecan market. Although not as dramatic, growers in Mexico, Australia and South Africa saw similar increases. While plantings increased worldwide to meet the anticipated growth in the Chinese market, nowhere were those increases as dramatic as those in Mexico and South Africa. With lower labor and production costs, and the ability to use growth hormones in their orchards, production in both countries soared.

While Mexico’s production has outpaced that of its northern neighbor three of the past four years, it is South Africa that is about to change how the pecan industry does business. A multicultural country of approximately 57 million people, it is the largest country in Southern Africa. Its constitution recognizes eleven official languages, and as such, is often referred to as the ‘rainbow nation.’ Blessed with three major ports strategically located along 1,553 miles of coastline—Durban, Cape Town and Port Elizabeth—the country is ideally situated to take advantage of one of the world’s busiest shipping lanes connecting two oceans.

At 471,445 square miles, South Africa is the 25th largest country in the world, about twice the size of France. The interior of the country, part of what is known as the central plateau, is primarily flat. The plateau is surrounded by the Great Escarpment extending from the northeast and running parallel to the coastline to the south, west and then to the northwest. Elevations generally vary from approximately 3,300 feet in the east to 6,900 feet in the west.

Ideally situated between 21 and 35 degrees south latitude, growing conditions in South Africa’s eastern provinces are similar to Georgia (Albany is at 31 degrees North latitude) while the western growing regions, particularly the Northern Cape, are similar to New Mexico and Arizona (Las Cruces is at 32 degrees North latitude).

While South Africa is considered to have a strong banking system, it is unfortunately plagued by an inefficient government bureaucracy, restrictive labor laws, a shortage of educated workers, political instability and corruption. The recently passed land reform legislation is a good example of the government’s efforts to placate its majority constituency with minimal thought to its implementation and long-term economic consequences.

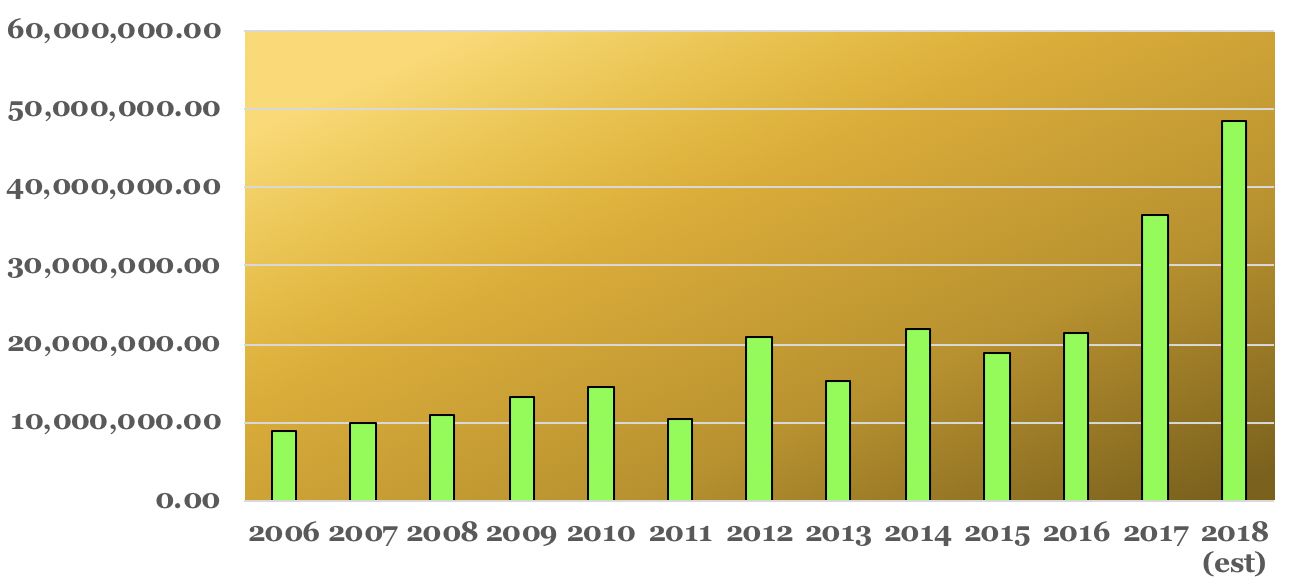

South African Pecan Production (inshell pounds by year)

The first commercial pecan plantings in South Africa occurred during the 1940s in the provinces of Natal and the Nelspruit/White River area of the Eastern Transvaal. The first commercial orchard, planted by Hall & Son’s, consisted primarily of ‘Elliot,’ ‘Moore,’ ‘Barton’ and ‘Choctaw.’[3] However, it wasn’t until early in this century that significant increases in production began to occur. Coincidently, plantings increased at about the same time as China’s appetite for inshell pecans began to skyrocket. Between 2006 and 2017, production increased over 413 percent from 8.8 million pounds to 36.4 million pounds.[4] If early estimates are correct, South Africa could harvest between 45 and 48 million pounds in 2018.[5]

Pecans are primarily grown in four areas of the country: the Northern Cape, the Eastern Cape, Natal and Limpopo. The farmers are hearty, experienced and in many cases, young. They have lived through tough political times and have learned to adapt to the ever-changing political landscape. Having cut their teeth on a variety of row crops, cattle, vineyards and some fruit trees, and in many cases having been forced to relocate hundreds of miles due to the country’s land-reform policies, they have become quick learners, students of both the U.S. and Mexican pecan industries, and have attempted to learn from the decades of knowledge, and mistakes, of their North American counterparts.

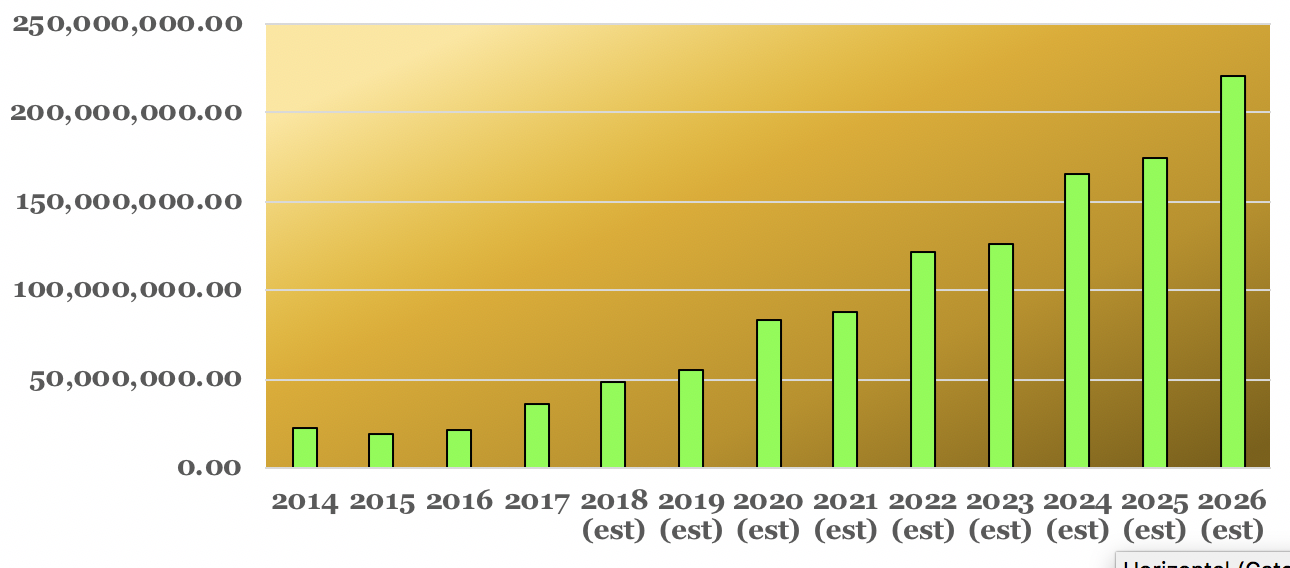

Projected South African Production (inshell pounds by year)

While plantings continue to increase across the country, the bulk of the new acreage is being planted in the Northern Cape area. Located in the North Central region of the country, it is an arid climate possessing many of the attributes of New Mexico and Arizona. The biggest difference—water. The area has an abundant source of water both from the Vaalharts Irrigation System and a good water table.

Focused around the cities of Upington, Prieska, Douglas and Hartswater, the area produces between 80 and 90 percent of the country’s pecans.[6] As one would expect, the predominant varieties are the same as those grown in the southwestern United States with many of the growers focusing on ‘Wichita,’ ‘Choctaw,’ ‘Navaho’ and ‘Western.’

As mentioned earlier, pecans are also grown in the Eastern Cape, Limpopo and Natal. Of the three areas, Natal accounts for a significant portion of the country’s remaining production. With growing conditions very similar to Georgia. Although the orchards are at a higher elevation, growers in this region of the country face many of the same problems as their Georgia counterparts—scab and pests to name just two. The predominant varieties are ‘Ukulinga,’ ‘Barton,’ ‘Sutex’ and ‘Choctaw.’[7]

In the past few years, plantings have also begun in the Ceres area of the Western Cape.

Based on current South African Pecan Nut Producers Association (SAPPA) estimates, there are approximately 62,500 to 75,000 acres of pecans planted in South Africa. At the current rate of planting, production could exceed 220 million pounds by 2026.[8]

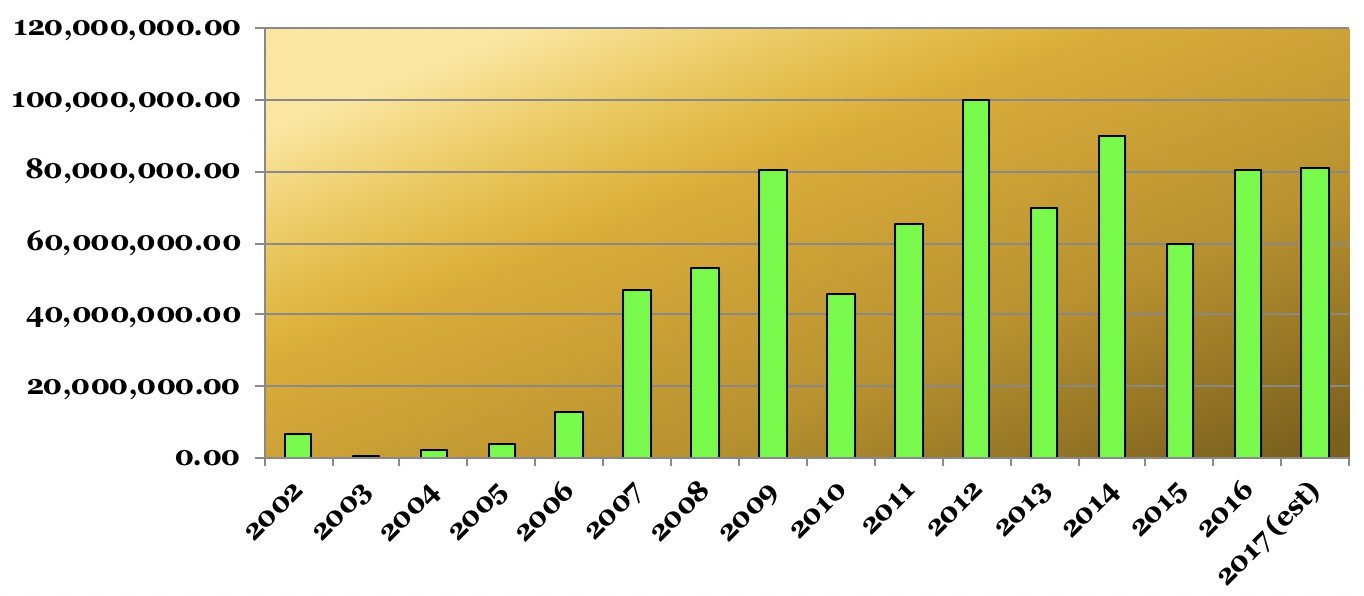

This brings us back to China. While China has been the main reason for the increase of worldwide pecan plantings, it has also been the reason for increased pecan prices, both for inshell and shelled kernels. Between 2003 and 2012, US pecan exports to China, including Hong Kong and Vietnam, increased from 835,544 pounds to 99,897,667 pounds (inshell basis).

U.S. Pecan Exports to China (inshell pounds by year)

Because of the nature of the Chinese economy, trader driven versus consumer driven, and the lack of understanding by the Chinese as to the relationship between the price of shelled kernels and the price of inshell, inshell prices increased almost 129 percent.[9] That increase, like a set of dominos, led to an increase in shelled kernel prices of 82.2 percent.[10]

Seventy percent of worldwide pecan sales are in the form of shelled kernels. As such, sales to China became a double-edged sword. The U.S. market, the largest buyer of shelled kernels, was forced to cut back on their purchases of shelled kernels as sales of inshell to China increased. In turn, increased grower profits led to increased plantings around the world and increased competition for a share of the China market.

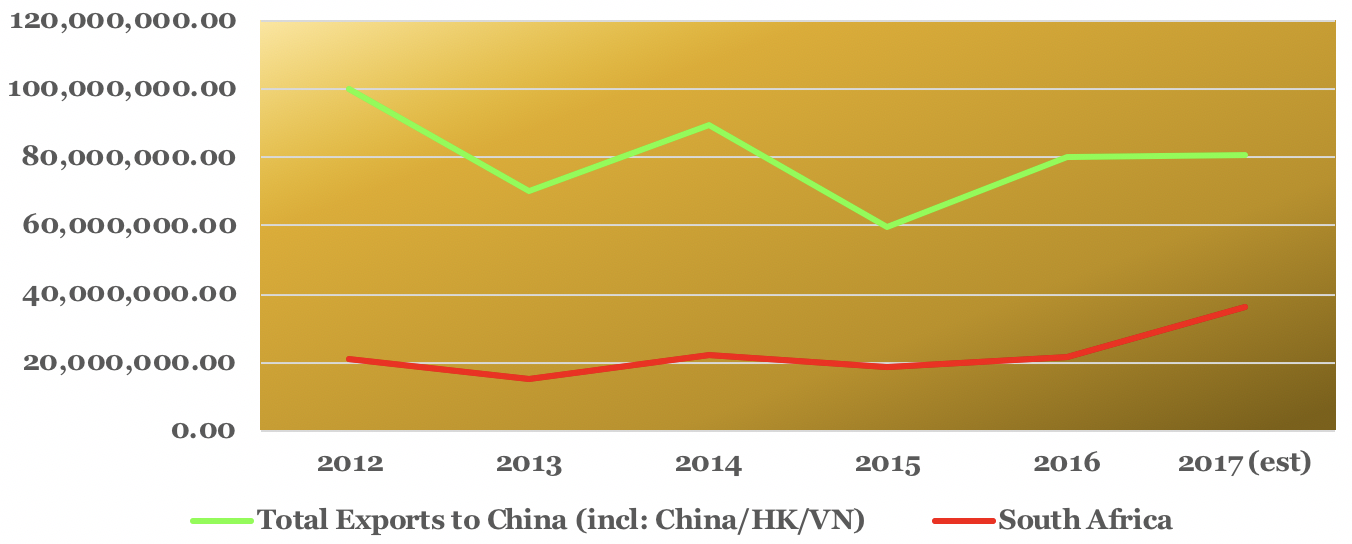

However, even Chinese traders have their limits. Near record inshell prices and China’s ability to switch consumers to cheaper walnuts have kept China from increasing its consumption of pecans. Since 2012, worldwide exports of pecans to China has remained flat, somewhere in the 120 and 140-million-pound range.[11] However, due to the increased number of inshell purchasing options, since 2012, U.S. pecan exports to China have continued to decline.[12]

U.S. Pecan Exports to China versus South African Production

Why is this important? Because of South Africa. For the past eleven years, U.S. growers have dictated world inshell prices, which, in turn, have dictated world shelled kernel prices. With few options to secure the volume of pecans needed to satisfy demand, China has been forced to buy the bulk of their pecans from the U.S. However, that is about to change. Since 2012, as South Africa’s production has increased, U.S. exports to China (including Hong Kong and Vietnam) have continued to decline. [13]

With their harvest occurring five months earlier than the U.S. or Mexico, and production costs approximately 60 percent lower than their US counterparts and approximately 30 percent below Mexico, it is not unreasonable to assume that this trend will continue. Other than China’s preference for ‘Desirables’ and ‘Stuarts,’ ‘Westerns’ and ‘Wichitas’ are the same whether grown in Mexico, South Africa, Australia or the southwestern U.S.

South Africa’s lack of a domestic pecan market or a viable shelling industry will also be key factors going forward. Eighty to eighty-five percent of South Africa’s production is currently being sold to China.[14] Having developed no other markets for their pecans, should China not dramatically increase their inshell consumption, price will play a greater role in China’s purchasing decisions. South Africa’s lower cost of production, as well as their proximity to China, will afford their growers the opportunity to profitably increase their share of the Chinese market at pricing levels the American, Mexican and Australian growers cannot economically match.

There are, however, two areas that could spell trouble for South Africa: the use of growth hormones on their trees and recently passed land reform legislation.

At one orchard in South Africa, this tree, seen with a number of nut clusters, was treated with 12 milliliters of Cultar to facilitate growth. (Photo by Dan Zedan)

The use of growth hormones, both in Mexico and South Africa, has become increasingly popular, especially on younger trees. Sold under several names, Cultar[15] is finding increased popularity among South African growers. While there is little, if any, data on the long-term impact on the trees, the short-term benefit is to slow the growth of the tree, thereby allowing more trees to be planted per acre while increasing nut production per tree. Although Cultar is banned in the United States, except for use in the landscaping and ornamental tree industries, neither the U.S. Department of Agriculture nor the Food and Drug Administration currently test for the presence of the chemical on pecans coming into the U.S. With inadequate independent data on the products possible health impacts, a change in the USDA’s or FDA’s position on the importation of Cultar treated pecans would have a significant impact on the number of pecans allowed into the U.S., both for Mexico and South Africa.

As for the recently passed land reform legislation, while there is a sense of cautious optimism among many growers as to the possible implementation of the law, there is still concern. Land reform in South Africa is not new. However, the current legislation differs significantly from the law that was enacted after the election of Nelson Mandela in 1994.

Under the old law, if it was determined that a white farmer owned land that had been improperly or illegally taken from a black South African, the land would be returned to its rightful owner with the farmer receiving fair compensation. It did not matter that the land may have been properly purchased by the farmer. All that mattered was the determination that at some point, either the British Government or the White Minority South African Government had taken the land. The process by which the land would be returned set-out specific guidelines as to how such a claim could be made, processed and adjudicated.

Unfortunately, recent changes in the political climate led to the passage of the new law. Under South Africa’s former President Jacob Zuma, government corruption reached epic proportions, so much so, that last year, the African National Congress (ANC) lost significant elections in both Johannesburg and Pretoria, their home base.

Realizing that they were losing the support of their electorate, the African National Congress (ANC) removed President Zuma from office on Feb. 15, 2018, and replaced him with Cyril Ramaphosa, an affluent black businessman and farmer. The new law, passed shortly after his election, is similar to the old law with one major exception; there is no provision for compensation.

Although the law has been passed, there are several hurdles that must be overcome before any land can be taken without compensation.

Why did I highlight “any”? It is my understanding that the new law is not specific to farmland. All land is subject to possible redistribution. Technically, this could include the bulk of the land currently occupied by the cities of Cape Town and Durban.

Next, before the law can be implemented, the country’s constitution would have to be amended. While there is currently a move to do so, at the moment, it has not. Assuming that the ANC is successful in amending the constitution, the law clearly states that the redistribution of any land cannot adversely impact a third party. Since approximately 80 percent of all the farms are “bonded,” i.e. have a mortgage or other lien, those farms could not be taken. Finally, since the government controls approximately 70 percent of the land in South Africa, 35 percent of which is currently non-productive, the government would distribute that land first.

According to recent comments made by South African President Ramaphosa, it is not anticipated that any privately-held land would be expropriated until after the 2019 National Election.[16] Considered a savvy businessman, President Ramaphosa understands the potential economic impact of losing the support of the country’s “white” minority. Because of this, many farmers are hopeful for a reasoned approach to repairing the economy, while addressing some of the country’s past injustices.

In closing, I am reminded of a recent marketing campaign run by our nation’s railroads, Operation Lifesaver. The goal of the campaign was to get the public to respect grade crossing markers and acknowledge their inability to gauge the speed of an oncoming train. However, even though people know that it is dangerous to do so, they continue to drive around grade crossing gates or ignore the red warning flashers, usually with catastrophic results. The same can be said about the pecan industry. There is a train coming and we cannot stop it. As such, we can either choose to ignore the warning signs or make sure that we are ready for its arrival.

[1] USDA NASS Noncitrus Nuts and Fruits-2012 Summary, July 2012; USDA Foreign Agricultural Service-July 2013 GATS Data

[2] USDA Foreign Agricultural Service-July 2013 GATS Data

[3] Mtebeni Valley Ranch, South Africa

[4] SAPPA-South African Pecan Nut Producers Association

[5] Golden Peanut and Tree Nut – South Africa

[6] SAPPA

[7] Ukulinga and Sutex are South African Varieties. Ukulinga is also used as the industry’s primary rootstock

[8] Golden Peanut & Tree Nut – South Africa

[9] USDA, Foreign Agricultural Service (FAS)

[10] Nature’s Finest Foods, Ltd.

[11] USDA, FAS, Agricultural Information Service-Mexico, Stahman Farms-Australia, Golden Peanut & Tree Nut – South Africa, Mtebeni Valley Ranch – South Africa

[12] USDA, FAS

[13] USDA, FAS, SAPPA, Golden Peanut & Tree Nut – South Africa

[14] SAPPA

[15] Trade name for paclobutrazol. Austar is a similar product

[16] Reuters Staff, World News, June 7, 2018